In the original post on ‘Taxation Options’ I provided the history of the ‘quest’ over many assemblies to address the very unpopular challenge of increasing taxation. During that time, there have also been various efficiency and cost-cutting drives too – and one of the major ones did achieve substantial savings of circa £30 million. Indeed, another one has just occurred prior to the Budget debate at the end of 2024 and a further exercise is planned during 2025 (this latter exercise will focus more specifically on how Universal Entitlement can be identified and to what extent Government should maintain its current portfolio of activities) This could be something of a game-changer, albeit likely to be very controversial since it could result in moving the burden of payment for currently subsidised Government services to individuals (user pays).

This is an important point to grasp. The quantum of funding needed to sustain the provision and known growth in demand (particularly in Healthcare) simply cannot be met by Government ‘efficiencies’. Growth in the economy would bring in more revenue via various taxes – if it means people earn more under our current taxation which is heavily slanted towards tax on earnings. However, it should not be overestimated how much impact productivity might have on taxes given that we do not tax business profits for many entities. An improvement in profits resulting from adoption of (for example tech or AI products), would not necessarily translate into more taxable income on employees. It should eventually find its way through tax on company dividends – if and when those are finally distributed. There is also the downside of increased use of AI/Tech – that a lot of administration-based employment could contract – or potentially disappear.

One myth that must be dispelled is that the demand for growth in services can be avoided without some level of increased taxation – unless Islanders are prepared to do without a lot of services – or as mentioned before – take on direct payment individually. There are some Deputies today who still will not accept this as an inevitability and believe that ‘Growth’ will suffice in combination with Government efficiencies. If that were true – we would need to see a growth percentage that would outmatch what China has achieved in the last decade. Frankly, that is unrealistic – with a longer runway or not.

Taxation considerations

So, returning to the historic recognition that many Assemblies have usually arrived at – taxation needs to be increased but has to be as fair as possible – essentially it has to be a progressive measure, plus – ideally, it should broaden the tax base so that we are not as dependent on earned income as we are today. It also goes without saying that if new measures lead to behavioural change that damages the current tax take – then such measures should be avoided – or substantially mitigated to minimise their impact. There are perhaps two other options to put into the mix – ‘death by a thousand cuts’ (a slew of minor taxes that are directed at individuals or sectors of the economy, such as motoring taxes and TRP), or a more broad-based approach that covers most households sufficiently ‘take a little from a lot’.

Consider too, what gets taken directly from your pay packet at source such as income tax or social Insurance (over which you have little choice) and taxes based on consumption or usage – which put more discretion in your hands about what you do with your disposable income (sales taxes). For those who have concerns about such things as Sustainability, the second option allows you freedoms that the first does not.

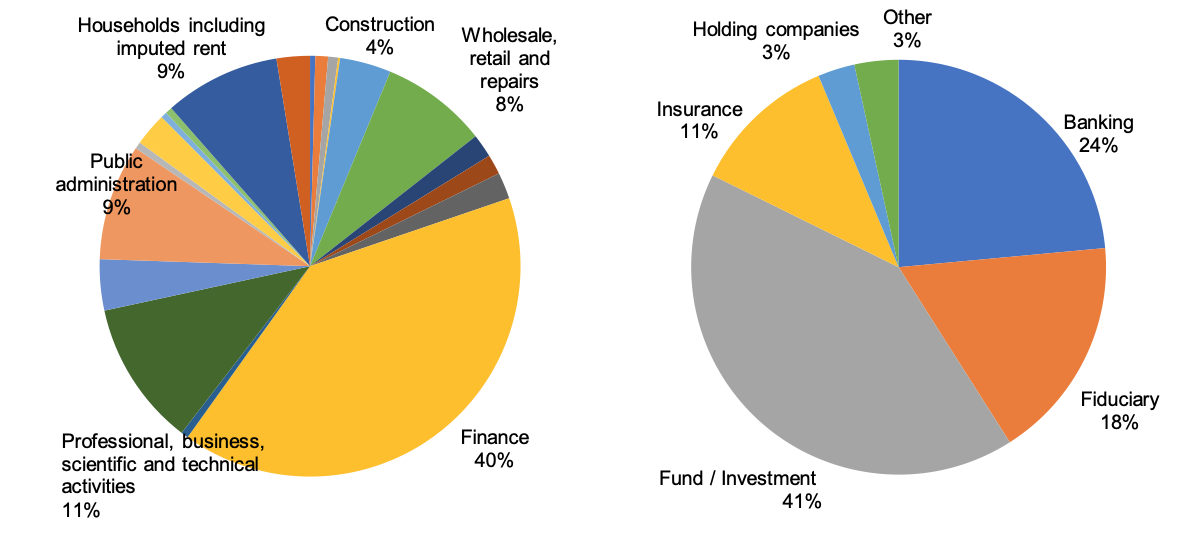

Context too is useful when trying to decide the best route to take. Islanders should probably already realise the significance of the Finance industry to our economy (particularly in respect of providing employment and thereby generating income taxes). The diagram below (taken from the EY Strategic Tax Review in September 2022) helps to illustrate exactly what different industries are contributing to our economy.

This concludes this part of the considerations of Taxation Options. In Part 3, I will look at the most recent outcome of this Assembly’s deliberations from the 2024 Budget debate which included changes to Income Tax, the introduction of a GST+ package and a debate over Territorial Tax.