“For too long, the States have scraped by on short-term solutions, unsustainable restrictions on infrastructure investment and stretching minor taxes and charges. There will always be a temptation to sustain this for just one more year, but at some point decisive steps are needed to secure our public finances. States of Guernsey Budget 2025, Executive Summary”.

The P&R 2025 Budget that was brought to the Assembly in October 2024 had two, linked objectives: it sought to introduce a rise in income tax (to 22%) for a 2-year limited period, which at this point in the term, would allow the incoming Assembly in June to have time to re-assess the longer term taxation needs in 2026 – generating nearly £60m towards the current deficit in the meantime. It also included an option for a GST+ to be introduced by 2027. In the event, the Assembly chose not to approve the interim Income tax proposal but did approve the GST+ commitment. Consequently, the rest of the 2025 budget proposals were approved but left unfunded – thereby worsening the structural deficit. This is an issue that candidates need to be cognisant of.

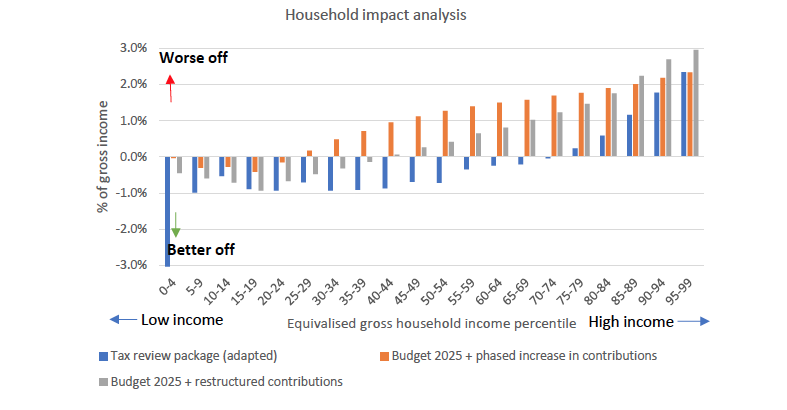

It was not an easy debate. It is likely however, that although the GST+ package had already been proposed 3 times before and failed each time, that the comparison with its impact upon the community in comparison with a similar illustration for Income tax might have been the deciding factor. Deputies had not seen the more extensive piece of work on the impact of Income tax before. Here was the comparison and for clarity, the orange bars represented the impact of an Income Tax (and prior-agreed continuing increase in Social Insurance), whilst the blue bars showed how GST+ would impact.

Due to the extensive overhaul of the Social Insurance system that would be part of the introduction of GST and a raft of other measures, it will be apparent that most households are better off. However, this comes with some other impacts that need to be realised. Firstly, the onus of collecting the tax is largely upon business. That said, if many businesses are not paying a tax on profits, then that is maybe a reasonable price to pay. Secondly, it will be more costly to collect than Income tax, but the quantum of income in relation to the amount of cost makes it relatively insignificant. Thirdly, it will take 2 years to implement due to the changes and training required. Fourthly, it will be inflationary for the first year (based on the Jersey experience back in 2008). In mitigation however, it does bring in some £14 million from Visitors and Corporates that of course, Income tax does not capture. But Income Tax can be introduced almost immediately and is certainly a tax that pretty much everybody understands. GST+ does have the singular advantage of diversifying the Island’s tax base however.

A major concern that agreeing to this fairly contentious consumption tax at this point in the 2025 Term, is that a new Assembly could decide to remove it. – or not introduce it. But it should be noted (also from the Executive Summary in the 2025 Budget proposals) “But we are not pretending that the measures in this Budget solve our financial problems.” In short, 2% on Income Tax would be insufficient to do so. But this is where a further factor comes into play – our competitive position in relation to places like Jersey and the Isle of Man (who both have a Consumption Tax already). It is also opportune at this point to mention another option that has continually been raised as an alternative – that of a Territorial Tax.

This is actually a two-edged sword because on the one hand it captures tax on all business profits made in Guernsey but it also is not something that our competitors currently do. Furthermore, it would almost certainly have to be considered by the International Code of Conduct body who could well ‘grey list’ us until they make a judgement on it. It is not therefore without risk. Raising the basic rate of tax or introducing a Consumption tax is entirely a decision for ourselves in comparison. That said, at this time of asking, it did receive more votes than it had historically.

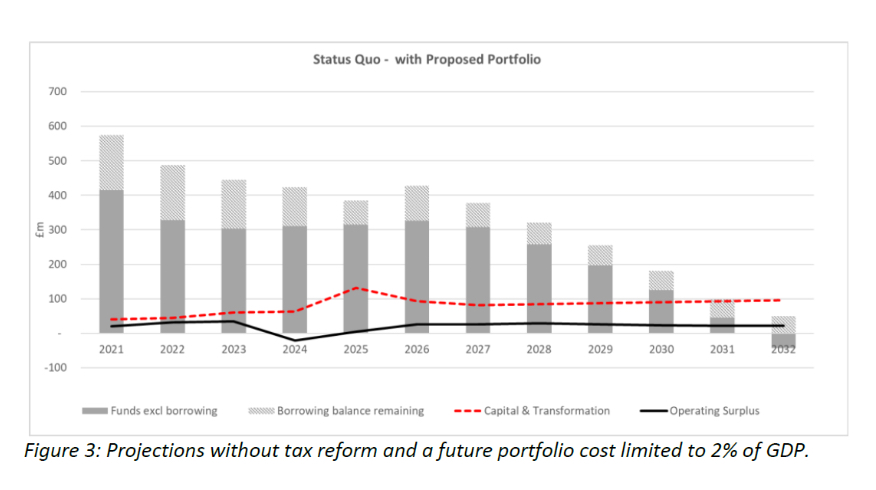

The fact that the 2025 Assembly have committed the next States to the GST+ proposals may well make it an election issue for some Islanders (and Candidates). However, should any candidate seek to be elected on the basis of removing this commitment – they will need to be armed with an alternative proposal to address the shortfall in Government funds, which comprise of a growing structural deficit of circa £50 Million per annum and a raft of outstanding infrastructure projects of at least a Billion pounds – but with next to no capital to cover that. The below illustration taken from the 2025 Infrastructure review indicates that without substantial tax reform, Government reserves will have been exhausted and the Island would be in a deficit position by 2032 – and that does not bear thinking about.